Smart Alternatives to Money Market Funds: Maximize Your Cash as Interest Rates Drop

As interest rates begin to come down, many investors are reassessing where to park excess cash. For some time, money market funds, high-yield savings accounts, and other short-term cash instruments have provided safe and attractive returns. However, with rates now trending lower, the appeal of these traditional cash products is fading. It’s time to explore alternatives that can offer better returns without compromising too much on liquidity or safety.

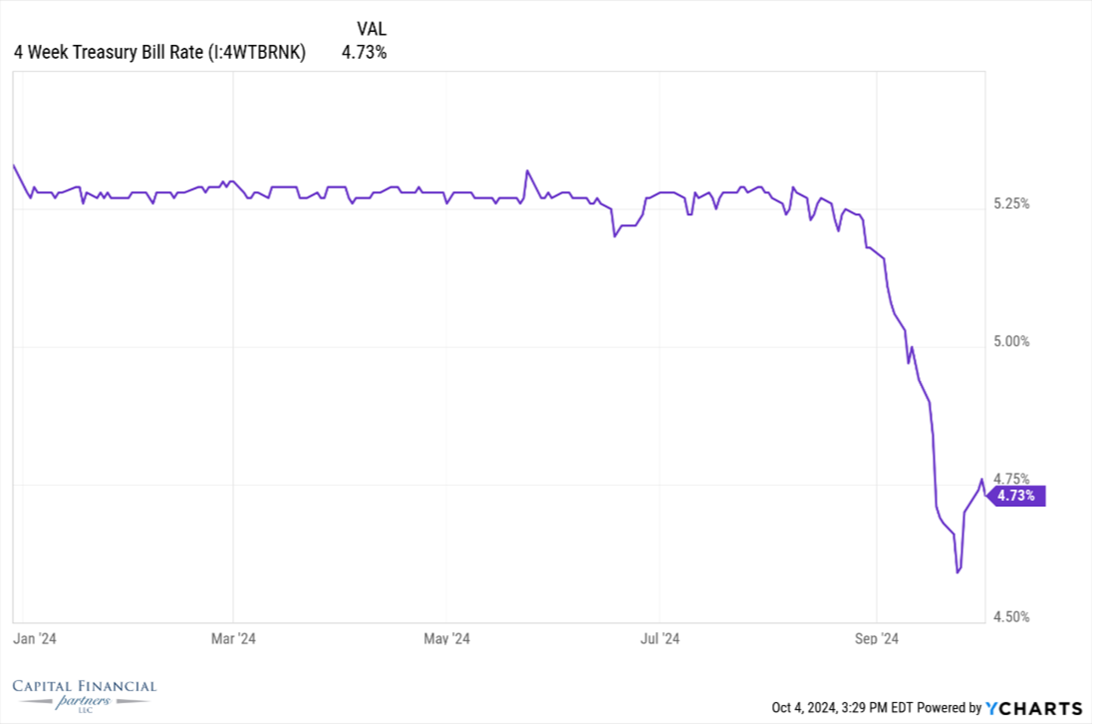

Why Money Market Funds Are Losing Appeal

Money market funds have been a reliable option for investors who want to earn more than a traditional savings account while maintaining liquidity. These funds invest in highly liquid, short-term debt securities and offer relatively stable returns. However, they are directly tied to short-term interest rates, which means as rates fall, so do their yields. While they will continue to offer liquidity, the returns may no longer be competitive as the interest rate environment shifts.

Personally, I’ve been waiting for the 4.5% rate on my savings account to decrease dramatically. Fast forward to Tuesday, I woke up to see the result: 2.7%.

In a falling interest rate scenario, the main drawback of money market funds is that they can’t lock in higher yields. Their returns fluctuate with market conditions, and in a declining rate environment, they may no longer offer the same level of income that attracted investors when rates were higher. As yields drop, it’s worth looking at other fixed-income options or even considering different asset classes altogether.

Consider Bond Ladders for Consistent Returns

One viable alternative to money market funds in a lower-rate environment is a bond ladder. A bond ladder involves purchasing bonds with staggered maturities. This strategy provides several benefits. First, by locking in bond yields at today’s still relatively higher rates, you can secure better returns than waiting for future rate cuts. Second, as each bond matures, you can reinvest the proceeds into new bonds at prevailing rates. This staggered approach reduces interest rate risk and ensures ongoing income, providing a more stable return than a money market fund would in a declining rate environment.

Bond ladders can be built with government bonds, municipal bonds, or corporate bonds, depending on your risk tolerance. Government bonds, especially Treasuries, offer safety, while municipal bonds provide tax advantages. Corporate bonds can offer higher yields but come with more credit risk. Customizing the bond ladder to your financial goals and time horizon is key.

Ultrashort Bond Funds as a Flexible Option

Another alternative to money market funds is ultrashort bond funds. These funds invest in bonds with very short durations, typically less than one year, and aim to provide higher returns than money market funds while still maintaining liquidity. Because ultrashort bond funds invest in short-term securities, they are less sensitive to interest rate changes than longer-term bond funds, which makes them a relatively safe choice in a falling rate environment.

While ultrashort bond funds do carry more risk than traditional money market funds, their exposure to a diversified pool of bonds can help mitigate the risk of any one bond defaulting. Additionally, these funds provide more yield potential, especially as short-term interest rates start to decline. Investors who are willing to accept a slight increase in risk can find ultrashort bond funds an attractive middle ground between safety and return.

Certificates of Deposit (CDs) for Stability

Certificates of deposit (CDs) are another alternative for those seeking to preserve capital while locking in a fixed return. In a declining interest rate environment, locking into a CD now can be an excellent strategy, as it allows you to secure today’s higher rates before they drop further. CDs come in varying terms, typically ranging from three months to five years, allowing you to choose a term that aligns with your liquidity needs.

One thing to keep in mind with CDs is their lack of liquidity compared to money market funds or savings accounts. Once you lock into a CD, your money is tied up for the duration of the term, and early withdrawal penalties could apply. However, many investors use a CD ladder, similar to a bond ladder, to stagger maturities and maintain some liquidity. This way, as each CD matures, you can reinvest at prevailing rates or access your cash as needed.

Other Fixed-Income Investments for Lower Risk

For those seeking additional fixed-income options beyond CDs, floating-rate bonds or Treasury Inflation-Protected Securities (TIPS) can also provide a buffer against the effects of a declining rate environment. Floating-rate bonds, as the name implies, have interest payments that adjust with prevailing interest rates, providing some protection in case rates fluctuate. This makes them more attractive than traditional fixed-rate bonds, particularly if rates move unpredictably.

TIPS, on the other hand, are government bonds designed to protect against inflation. While TIPS yields tend to be lower, their principal value adjusts with inflation, offering a safeguard against the erosion of purchasing power over time. In a lower interest rate and inflationary environment, TIPS can provide a balance of safety and income, especially for those with a longer time horizon and conservative risk profile.

Tailoring Your Strategy for a Lower Rate Environment

As rates continue to decline, it’s important to stay proactive and adjust your cash management strategy to reflect the changing environment. Money market funds may no longer provide the returns you need, but there are many alternatives that can offer both income and growth potential. Whether you opt for a bond ladder, ultrashort bond funds, dividend-paying stocks, or REITs, the key is to diversify your portfolio and balance risk and reward based on your individual goals.

By exploring these money market alternatives, you can stay ahead of the interest rate curve and make sure your excess cash is working as efficiently as possible in today’s evolving financial landscape.